By ESG Analyst Chloe Stoneburgh

It is undeniable that China will play a critical role in global efforts to combat climate change as they emit 27% of global carbon dioxide and a third of the world’s greenhouse gases. Their large emissions of greenhouse gases and heavy exposure to climate risks create an increased sense of urgency for action in the green transition. Without successfully transitioning to a low-carbon economy, China could see a loss of their GDP of up to 2.3% as early as 2030 and global climate goals would be impossible to meet.

However, China is well positioned to meet climate commitments as demonstrated by their Country Climate and Development Report for China outlining how to turn climate change into an opportunity. Specifically, they have pledged to have CO2 emissions peak before 2030 and achieve carbon neutrality before 2060. China’s emissions are underway to peak by 2025, five years ahead of its 2030 target, but policies beyond that target and their target reductions are lacking. The Climate Action Tracker deems China’s overall action as highly insignificant with limited concrete climate policy or plans to keep emissions in line with its 2060 goal.

An essential part of transitioning to a lower carbon economy is financing it. Despite the consensus that China’s climate policy is lacking, they have aimed to establish themselves as a leader in green finance. This is where green bonds become an essential consideration.

Green bonds are a type of fixed-income instrument used to raise money for climate and environmental projects. These are usually asset-linked bonds backed by the issuing entity’s balance sheet. They represent a broad category of instruments designed to raise funds for environmental projects and require the issuer to commit to providing information on the projects supported by the proceeds.

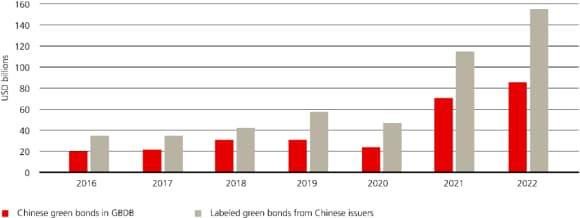

China’s green bond market has seen explosive growth as seen through the below chart showing the growth of green bond issuance from 2016 to 2022. Because of this rapid growth, China is the supplier with the largest volume of green bonds at 489 billion USD.

Chart 1: China’s green bond issuance

Supportive policies have contributed to this rapid expansion. Specifically, in 2018 the People’s Bank of China decided to include green financial bonds as eligible for its Medium Term Lending Facility (the rate at which the central banks lend to big commercial banks) as priority over other financial bonds (Banque de France). Other local government initiatives have contributed to the success such as the provincial government of Jiangsu providing an interest subsidy of 30 percent toward green bonds (International Monetary Fund).

This poses the essential question of where the disconnect lies between the financing of the green transition and actual climate action. One answer could be due to the lack of alignment with international green bond standards.

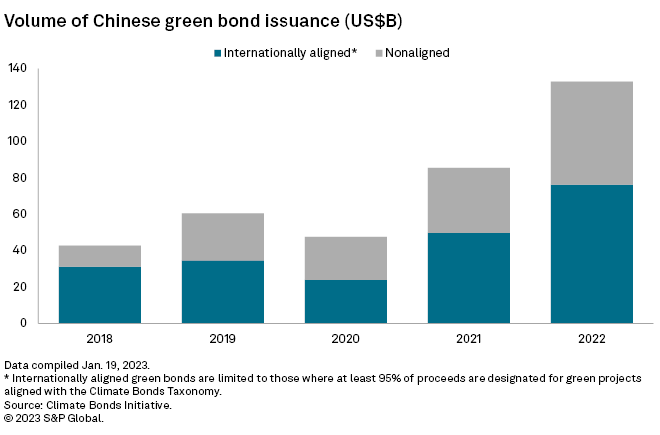

Despite policy support, large gaps remain in these bonds’ ability to align with international standards. Guidelines are essential in the green bond market to avoid the practice of using unsubstantiated claims of the financial product as environmentally friendly. The International Capital Markets Association (ICMA) created and regularly updates the Green Bond Principles to support transparency. Chinese green bonds are required to meet China’s Green Bonds Principle which is largely in alignment with the ICMA framework. Yet, non-aligned bonds, with some key differences from the ICMA standards, account for a substantial portion of its total green financing (S&P). For example, Chinese standards allow for clean coal projects to be financed by green bonds which do not align with international standards. Moves are being made to continue to standardize and align the international market which will ultimately attract a wider pool of capital. Yet, the pace of this alignment could dictate the success of these programs.

Chart 2: Volume of green bonds with international alignment

The green bond market is still a relatively young financial instrument, so the contribution to the energy transition is still largely unproven. Positive data is beginning to reveal itself such as the Climate Policy Initiative reviewing the reporting data of 311 of China’s green bonds to find most notably that 52.6 million tons of CO2 had been avoided annually and over 11 GW of clean energy had been deployed. Yet, with hundreds of billions of dollars being mobilized towards the environmental movement but a relatively negligible impact, it will be interesting to see if it will deliver significant environmental benefits in the coming years.

Overall, despite the rapid growth of China’s green bond market, the effectiveness of this financial instrument in delivering significant environmental benefits remains to be fully realized, emphasizing the ongoing need for international alignment and scrutiny to promote significant climate action in one of the world’s largest players.